Parking revenue sits inside most REIT portfolios already. It appears on the rent roll, flows into NOI calculations, and gets capitalized alongside every other income line. This all happens even though anyone is rarely managing revenue actively.

That disconnect is important because parking behaves differently from every other real estate income type. Leases lock in rates for years., but parking rates can change today. When demand shifts, a well-managed parking asset can capture that shift within hours. A poorly managed one won't notice for months, if ever.

For asset managers who treat parking as infrastructure rather than an income-producing asset, the cost of that posture shows up directly in NOI, and in the asset value built (or not built) on top of it.

How parking fits into institutional portfolios.

Within REIT portfolios, parking typically appears in one of two forms:

Facilities attached to core assets: Garages beneath office towers, parking supporting mixed-use or hotel properties. Demand is driven by the primary asset, like commuters for office, overnight guests for hotels, short-stay visitors for retail. That built-in demand produces stable revenue, but stability and optimization aren't the same thing. In most attached facilities, pricing rarely changes regardless of what's actually happening with occupancy.

One under-appreciated advantage: parking revenue stays flexible even when the rest of the asset doesn't. A partially leased office building still has a full garage. Parking rates can respond to real demand even when lease rates can't.

Stand-alone parking portfolios: Performance here depends entirely on how well the facility attracts, prices, and retains parkers. Without active management, these assets often run on static rates and minimal marketing efforts.

Why parking underperforms.

Parking underperformance is often not a demand problem. The gap is operational, and it comes down to a mismatch in management rhythm.

Parking attached to larger assets inherits those assets' slow cycles: annual lease reviews, quarterly reporting, multi-year capital plans. That rhythm makes sense for the core asset. It doesn't work for parking, where demand shifts daily and pricing decisions have an immediate revenue impact.

When parking runs on that slow rhythm, a few things happen:

- Pricing stays flat because no one is adjusting it

- Reporting arrives late, as monthly summaries come long after the opportunity to act has passed

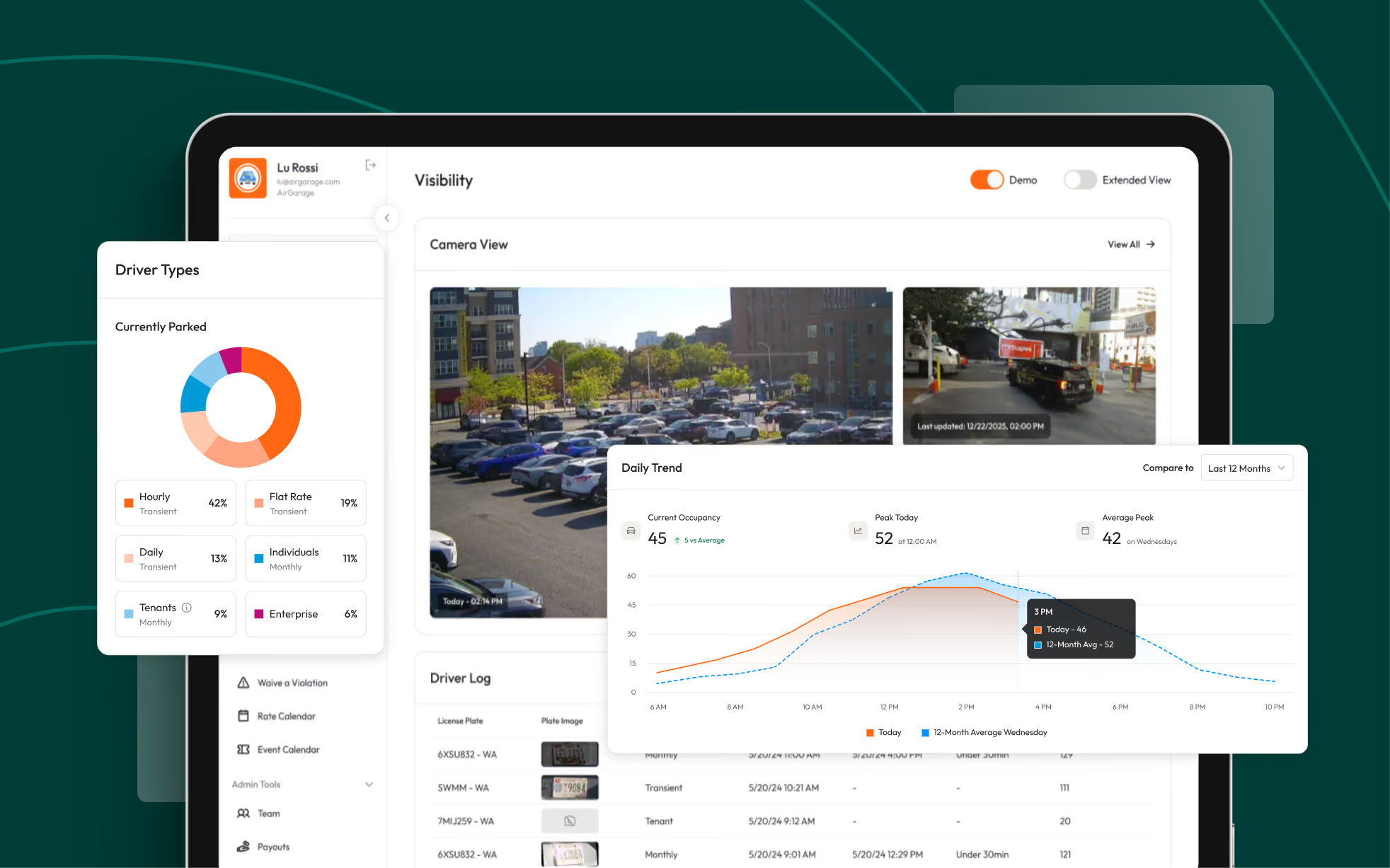

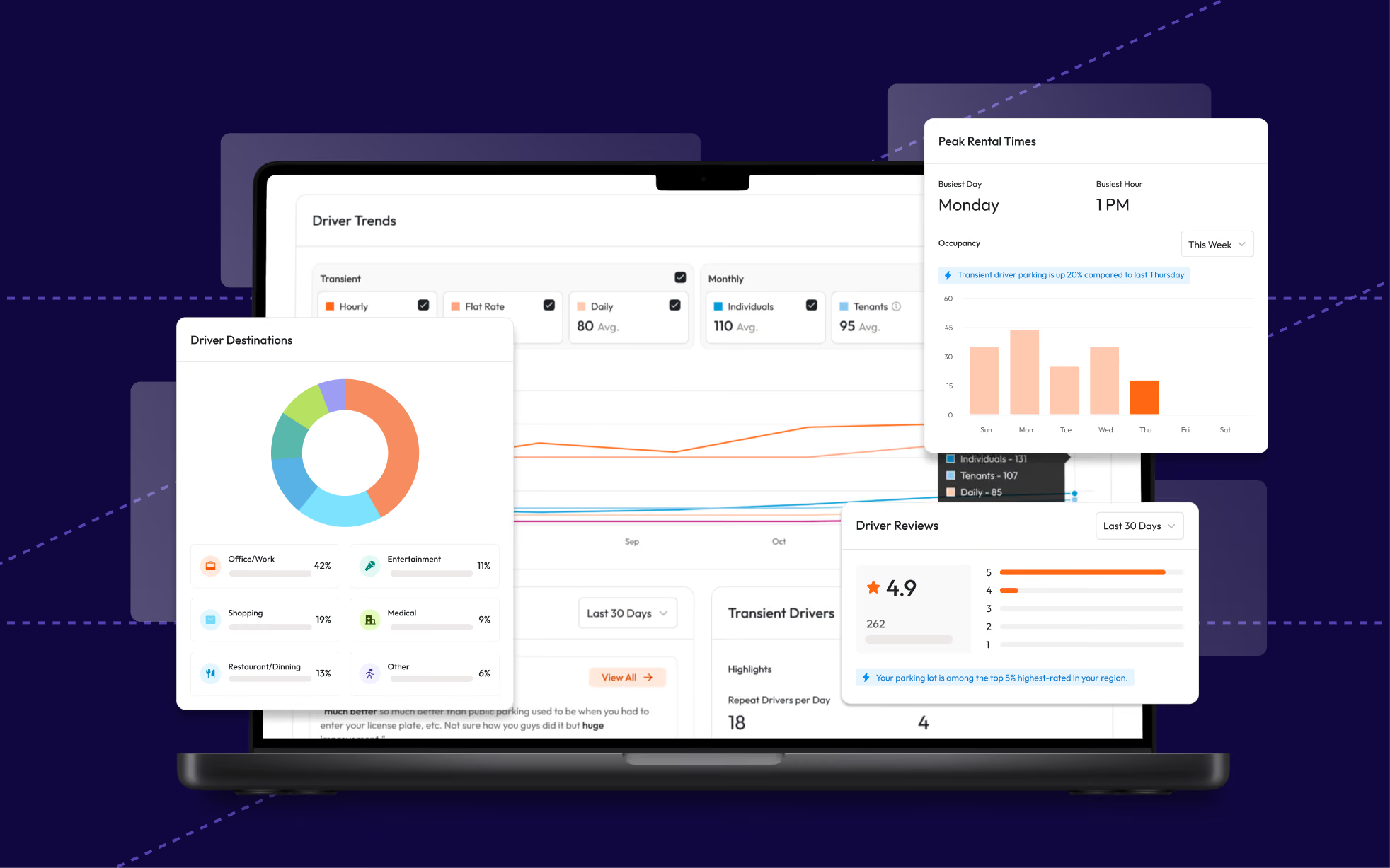

- Occupancy patterns go unanalyzed because there's no system watching them in real time

The result is stagnate asset performance.

What changes with active management:

- At BPG 360, limited visibility into what was driving performance across four Wilmington garages kept results static. After shifting to dynamic pricing and real-time data, parking NOI increased up to 30% across multiple assets in the first year.

- At 75 Saint in Boston, a 185-space garage had minimal monthly utilization and no transient strategy. Dynamic pricing and targeted marketing grew total revenue 200% within a year. The asset didn't change. Demand didn't change. A new pricing strategy unlocked the revenue.

How parking income fits within REIT rules.

Parking revenue can qualify as "rents from real property" under REIT income tests, but qualification depends on how the facility is operated. Asset managers should coordinate with tax and accounting advisors before restructuring parking operations.

The two primary income thresholds:

- At least 75% of gross income must come from real estate sources, including rents from real property

- At least 95% must come from real estate and other passive income categories like interest and dividends

Rent from real property means income received for the use or occupancy of real estate, not income from active services. In parking, that typically means customers pay for the right to park while the REIT handles standard landlord functions.

When income qualifies without structural complexity.

Unattended facilities where the REIT performs basic landlord functions generally qualify as rent. The structure stays straightforward.

When it gets more complex.

Reserved spaces, staffed operations, or public parking with active services require more care. If those services are provided directly by the REIT rather than an independent contractor, the income may not qualify as rent under REIT rules.

Two common structures for managing tax risk.

- Independent operators: REITs typically run active parking services through a parking management agreement. The economic arrangement may look similar, but the operating structure determines how income is treated. For institutional assets with staffed operations or public access, this is usually the cleaner path.

- Taxable REIT subsidiaries (TRSs): A TRS is a separate taxable entity owned by the REIT that can house service-based operating activities without affecting REIT income qualification, subject to limits on the proportion of REIT assets held in that structure.

In both cases, maintaining a true arm's-length relationship with the operator and reviewing income treatment regularly with tax and accounting advisors is essential.

Operating model decisions.

Once income qualification is understood, then the decision is who runs the facility and under what structure. This affects revenue performance, reporting visibility, and compliance alignment across the portfolio.

When self-operation works.

Self-operation is viable in narrow situations:

- Small, unattended facilities

- Exclusive tenant use with limited pricing complexity

- Single-property portfolios without need for cross-portfolio consistency

Where it breaks down at scale.

- Pricing, enforcement, and reporting decisions need to be consistent across properties, which is difficult to maintain when each site operates independently

- Managing parking internally requires pricing expertise and real-time systems that most institutional teams don't have in place

- Without centralized data, most facilities end up reviewing results after the fact rather than adjusting as demand changes

What to look for in a third-party operator.

An operator built for institutional portfolios needs to do more than handle day-to-day operations:

- Qualifies as a true independent contractor under REIT rules

- Provides centralized, real-time performance data across all properties

- Actively manages pricing, not just maintains it, so revenue reflects actual demand

- Aligns incentives with ownership through a revenue-share model

The operating model and the technology behind it need to work together. Real-time data is only useful if someone is acting on it. Dynamic pricing only works if enforcement supports it. When those pieces are disconnected, performance gaps persist even with better tools in place.

What active management actually produces.

The existing, untapped upside in most institutional parking portfolios isn't hidden in a capital project or a lease restructuring.

That's what makes parking unusual within a REIT portfolio. Most revenue improvements require time, capital, or both. Parking pricing and strategy can change quickly, and the revenue impact shows up fast.

And the math is straightforward:

A facility producing $500K annually looks very different capitalized at a 5% cap rate than one producing $650K. At REIT scale, that improvement compounds across every property in the portfolio.

For asset managers who already treat parking as part of the NOI calculation, the real question is whether the operating model behind it can actually grow that number. For most institutional parking, it can, it just isn't yet.

AirGarage helps REITs manage parking as a portfolio-level revenue strategy. Our platform gives asset managers real-time visibility across every property, while our team actively manages pricing, enforcement, and demand strategy so performance compounds over time. Explore our case studies to see how institutional portfolios have achieved meaningful NOI growth by managing parking as an asset.

Discover Asset Intelligence

Connect with one of our parking experts to learn more about how AirGarage proactively drives revenue, eliminates operational burden, and gives owners real-time visibility into their asset's performance.